The Disclosure Regulation, also referred to as the Sustainable Finance Disclosure Regulation (SFDR), is a set of rules for financial market participants such as AIFMs and UCITS managers, investment companies providing portfolio management services and financial advisers, including persons and companies providing investment advice ('investors').

The rules require investors to disclose information about the sustainability risks and opportunities associated with their products and their own sustainability practices.

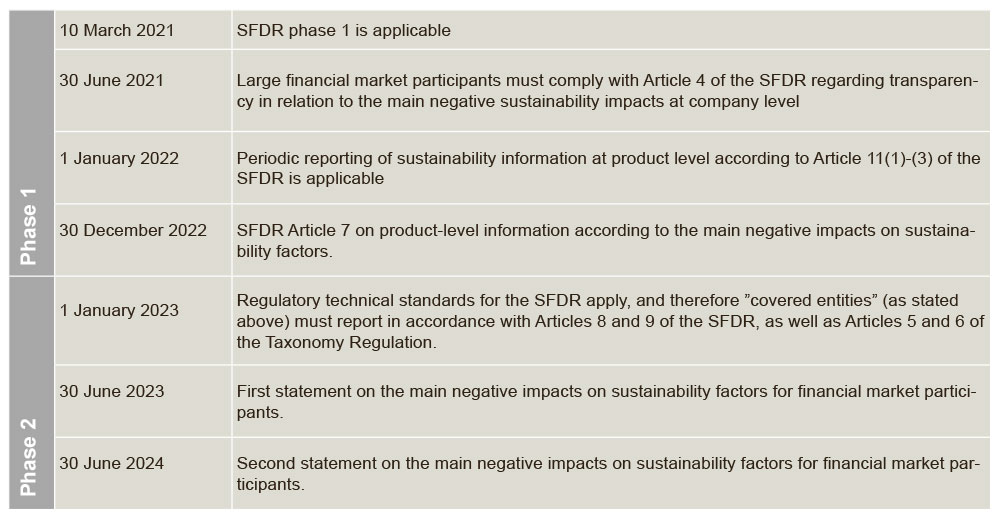

The Disclosure Regulation has been implemented in several phases, with different requirements coming into force at different times.

- Phase one, which sets out the most general disclosure requirements, became effective on 10 March 2021.

- Phase two, which includes the so-called Regulatory Technical Standards (RTS) containing detailed specifications of the content, methodology and presentation of certain information in the Disclosure Regulation, became effective on 1 January 2023.

Disclosure requirements

Under the Disclosure Regulation, investors are required to disclose information about their sustainability-related activities. This includes their policies for integration of sustainability risks into their investment activities as well as the impact of their activities on sustainability factors.

This information must be presented at both company and product level and must be presented in a clear, concise and balanced manner. It is crucial that investors and other stakeholders have access to up-to-date information, which is why regular reporting is required.

According to the regulation, the information must be available in different contexts and through different communication channels. Certain information must be disclosed in investors' annual report, on their official website and in marketing material which they use to promote their financial products.

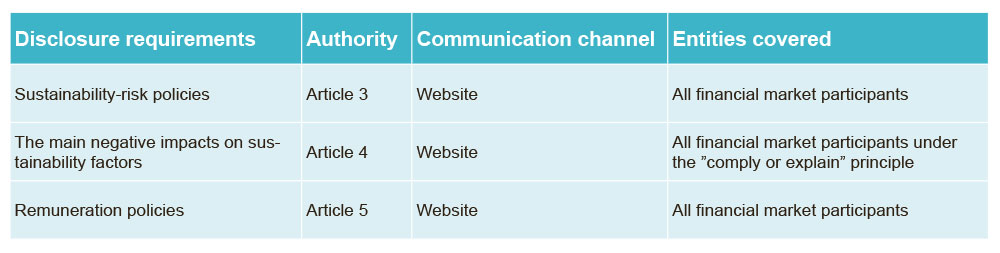

Disclosure requirements at company level

At company level, financial market participants must publish their policies for integration of sustainability risks into their investments on their website. In addition, in line with the 'comply or explain' principle, they must indicate whether they take into account the

main negative impacts on sustainability factors. If so, they must publish a statement on their due diligence policies in this connection. Finally, the company's remuneration policy must be disclosed.

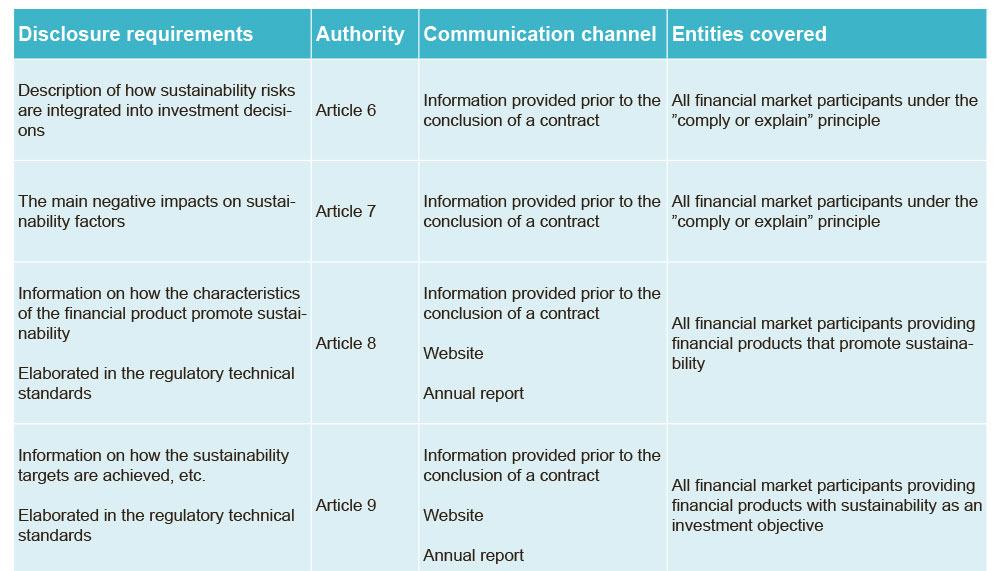

The disclosure requirement at product level

The scope of the product-level disclosure requirement depends on whether the financial product promotes sustainability or whether it has sustainability as the investment objective. In all cases, financial market participants are required to disclose, in accordance with the 'comply or explain' principle, whether they consider sustainability risks to be relevant in their investment decisions. If so, they must disclose how these risks are integrated into their decision-making process.

If the financial product promotes sustainability (Article 8), additional information must be provided on how the product contributes to sustainability. If the financial product has sustainable investments as its objective (Article 9), information must also be provided on how this objective will be achieved.

This information must also be published on the websites of financial market participants and reported in their annual reports.

Categorisation of the products

As mentioned, an Article 9 product must have sustainability as its investment objective. This means that the underlying assets of the financial product, such as a fund, are assumed to be sustainable economic activities. For example, if an Article 9 fund has the reduction of CO2 emissions as its objective, the fund's climate targets must be in line with the ambitions of the Paris Agreement.

In addition, all assets in Article 9 funds must fulfil the 'do no significant harm' principle. This means that a company that contributes to the green transition, but whose production harms the environment in a significant way, cannot be part of an Article 9 fund.

An Article 8 product promotes sustainability. This means that, as soon as the financial product complies with specific sustainability legislation, including international conventions and/or certain minimum standards, and the financial market participant markets this in its investment policy for that financial product, it is classified as an Article 8 product.

Financial products that do not fall under either Article 8 or 9 are referred to as Article 6 products.

The objective

The SFDR is an important step towards promoting transparency and the integration of Environmental, Social and Governance (ESG) considerations in the financial sector. By requiring companies and financial institutions to disclose information about sustainability-related risks and opportunities relating to their products, as well as their own sustainability practices, the SFDR helps promote responsible investment and encourages ESG factors to be taken into account in business and investment decisions.

We follow the regulation

At Horten, our ESG experts closely follow the development within the area and the regulation. We advise on a wide range of topics, including the scope of the regulation, implementation of ESG in the board and the company, including through double materiality analyses, and how companies can adapt to the new sustainability agenda with focus on ESG and ESG reporting. It is no longer a question of whether companies should take a position on ESG, but rather how and when to do so. Our experts are ready to assist companies navigate these complex and important issues.