28 November 2022, the Council of the European Union formally adopted the Reporting Directive, which was adopted by the European Parliament on 11 November 2022. The directive is an important step towards ensuring increased insight into the individual company's sustainability data and defining the company's task of collecting and communicating such data.

More extensive reporting requirements

The Reporting Directive amends and extends the existing Non-Financial Reporting Directive (NFRD), which has been implemented into section 99a of the Danish Financial Statements Act.

The existing rules on reporting of certain companies' impact on people and the environment are expanded. The companies will be obligated to publish information on their strategy and objectives along with the board of directors’ and the management’s role in relation to sustainability (“ESG”).

In addition, the principle of “double materiality” will be specified to make it clear that companies must both report information necessary to understand the impact of sustainability matters on companies and companies' own impact on people and the environment.

More companies will be covered

The Reporting Directive will also increase the number of companies covered - and thereby also the number of companies that are affected indirectly.

Denmark chose to expand the scope of application when implementing NFRD into section 99a of the Financial Statements Act. Consequently, the companies that are covered under the Reporting Directive – but were not covered under NFRD – are already reporting in Denmark.

Overall, the companies covered will report on sustainability in line with what is known from financial reporting, i.e. by way of definite calculations rather than merely soft wordings that may be reviewed by an auditor - and in this way be responsible in a different concrete manner for the company's social and climate footprint to the outside world.

European Sustainability Reporting Standards (ESRS)

The detailed reporting requirements under the Reporting Directive are laid down in a number of standards referred to as ESRS standards, which are expected to be adopted at different speeds. There is a need for common standards to ensure that the reported sustainability data are comparable and relevant - similar to reporting of companies' financial data.

The ESRS standards will specify the data to be reported by the companies within:

(E) environmental matters, including climate changes, water resources, circular economy, contamination, and biodiversity.

(S) social matters, including equal opportunities for all (i.a. gender composition and equal pay for equal work), employment matters, respect for human rights, etc.

(G) good corporate governance, including the management’s tasks in relation to corporate sustainability, business ethics and culture as well as the company's control and risk management in relation to sustainability risks.

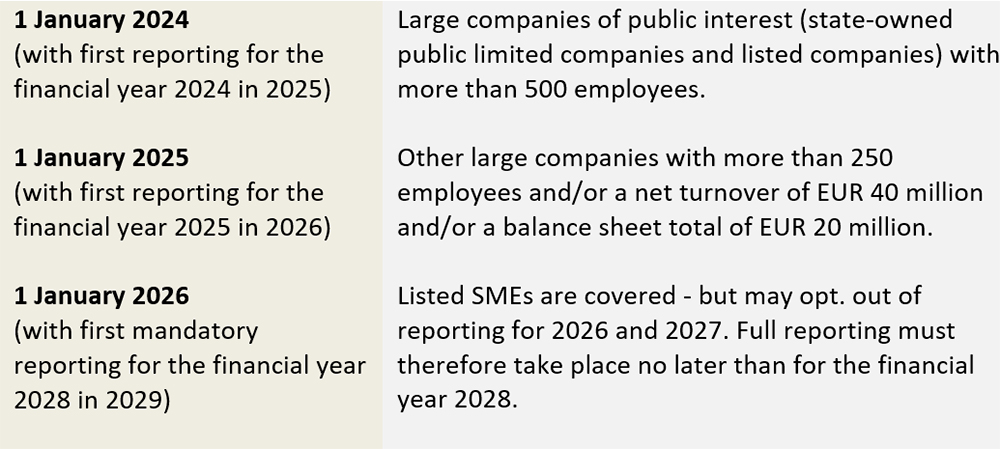

A directive taking effect at different speeds

The obligation to report the company's sustainability efforts and results enters into force at various speeds for the companies covered. This will give the companies time to prepare for the new way of reporting which requires comprehensive collection of relevant data.

It depends on the company's size (and whether it is listed) as to when it will be covered by the Reporting Directive:

Requirements throughout the company's value chain

In addition to the companies that are directly covered by the different rules on sustainability, a large number of companies are expected to be indirectly covered/affected by the regulation. This is due to the fact that reporting and data from sub-suppliers and other parts of the value chain will be a prerequisite for the ability of the companies covered by the regulation to comply with their reporting obligation.

The Reporting Directive is therefore expected to have significant implications for the requirements made in the value chain of an company - including for the suppliers.

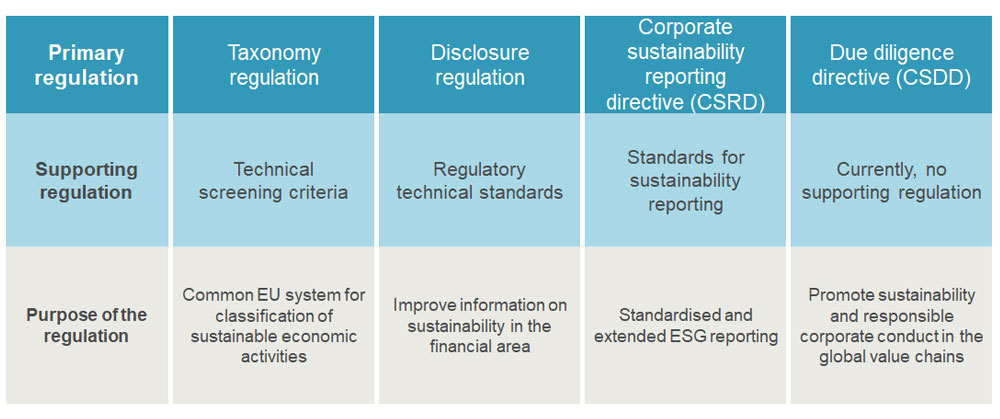

Outline of key ESG regulation

Each regulation and each directive are part of a major regulatory context, the intention of which is to place sustainability and ESG “on a formula” in the EU and the rest of the world.

The EU Corporate Sustainability Due Diligence Directive (CSDD) proposal is currently being considered by the Council of the European Union. The directive is expected to increase the demands for control of the entire value chain in relation to sustainability risks.

Horten’ ESG specialists monitor the development of the area and the regulation closely. We advise on all aspects; from the scope of the regulation, how ESG may be implemented in the board of directors and the company, and how companies can adapt to the new sustainability agenda in the form of ESG and ESG reporting. It is no longer a question as to whether companies should address ESG – but how and when.